Showing preview only (469K chars total). Download the full file or copy to clipboard to get everything.

Repository: waditu/tushare

Branch: master

Commit: 093856995af0

Files: 77

Total size: 446.5 KB

Directory structure:

gitextract_rwiezwpg/

├── .gitignore

├── .travis.yml

├── LICENSE

├── MANIFEST

├── README.md

├── issues/

│ ├── from_email.txt

│ └── from_sns.txt

├── requirements.txt

├── setup.py

├── test/

│ ├── __init__.py

│ ├── bar_test.py

│ ├── billboard_test.py

│ ├── classifying_test.py

│ ├── dateu_test.py

│ ├── fund_test.py

│ ├── indictor_test.py

│ ├── macro_test.py

│ ├── nav_test.py

│ ├── news_test.py

│ ├── ref_test.py

│ ├── shibor_test.py

│ ├── storing_test.py

│ └── trading_test.py

├── test_unittest.py

├── tushare/

│ ├── VERSION.txt

│ ├── __init__.py

│ ├── bond/

│ │ ├── __init__.py

│ │ └── bonds.py

│ ├── coins/

│ │ ├── __init__.py

│ │ └── market.py

│ ├── data/

│ │ └── __init__.py

│ ├── fund/

│ │ ├── __init__.py

│ │ ├── cons.py

│ │ └── nav.py

│ ├── futures/

│ │ ├── __init__.py

│ │ ├── cons.py

│ │ ├── domestic.py

│ │ ├── domestic_cons.py

│ │ └── intlfutures.py

│ ├── internet/

│ │ ├── __init__.py

│ │ ├── boxoffice.py

│ │ ├── caixinnews.py

│ │ └── indexes.py

│ ├── pro/

│ │ ├── __init__.py

│ │ ├── client.py

│ │ └── data_pro.py

│ ├── stock/

│ │ ├── __init__.py

│ │ ├── billboard.py

│ │ ├── classifying.py

│ │ ├── cons.py

│ │ ├── fundamental.py

│ │ ├── globals.py

│ │ ├── indictor.py

│ │ ├── macro.py

│ │ ├── macro_vars.py

│ │ ├── news_vars.py

│ │ ├── newsevent.py

│ │ ├── ref_vars.py

│ │ ├── reference.py

│ │ ├── shibor.py

│ │ ├── trading.py

│ │ └── trendline.py

│ ├── trader/

│ │ ├── __init__.py

│ │ ├── trader.py

│ │ ├── utils.py

│ │ └── vars.py

│ └── util/

│ ├── __init__.py

│ ├── common.py

│ ├── conns.py

│ ├── dateu.py

│ ├── formula.py

│ ├── mailmerge.py

│ ├── netbase.py

│ ├── store.py

│ ├── upass.py

│ └── vars.py

└── whats_new.md

================================================

FILE CONTENTS

================================================

================================================

FILE: .gitignore

================================================

# Byte-compiled / optimized / DLL files

*.log

*.swp

*.pdb

.project

.pydevproject

.settings

__pycache__/

*.py[cod]

# C extensions

*.so

# Distribution / packaging

.Python

env/

build/

develop-eggs/

dist/

downloads/

eggs/

source/

baks/

lib/

lib64/

parts/

sdist/

var/

docs/

*.egg-info/

.installed.cfg

*.egg

# PyInstaller

# Usually these files are written by a python script from a template

# before PyInstaller builds the exe, so as to inject date/other infos into it.

*.manifest

*.spec

# Installer logs

pip-log.txt

pip-delete-this-directory.txt

# Unit test / coverage reports

htmlcov/

.tox/

.coverage

.cache

nosetests.xml

coverage.xml

# Translations

*.mo

*.pot

# Django stuff:

*.log

# Sphinx documentation

docs/_build/

docs/*.md

docs/bin

.idea/

# PyBuilder

target/

#Visual Studio Environment

*.pyproj

*.sln

.vs/

#Vim Environment

tags

*~

================================================

FILE: .travis.yml

================================================

language: python

python:

# We don't actually use the Travis Python, but this keeps it organized.

- "2.7"

# "3.3"

- "3.4"

install:

- sudo apt-get update

# We do this conditionally because it saves us some downloading if the

# version is the same.

- if [[ "$TRAVIS_PYTHON_VERSION" == "2.7" ]]; then

wget https://repo.continuum.io/miniconda/Miniconda-latest-Linux-x86_64.sh -O miniconda.sh;

else

wget https://repo.continuum.io/miniconda/Miniconda3-latest-Linux-x86_64.sh -O miniconda.sh;

fi

- bash miniconda.sh -b -p $HOME/miniconda

- export PATH="$HOME/miniconda/bin:$PATH"

- hash -r

- conda config --set always_yes yes --set changeps1 no

- conda update -q conda

# Useful for debugging any issues with conda

- conda info -a

before_script:

- conda install --yes python=$TRAVIS_PYTHON_VERSION numpy scipy pandas matplotlib lxml pytesseract

- python setup.py install

script:

- python test_unittest.py

================================================

FILE: LICENSE

================================================

Copyright (c) 2015, 挖地兔

All rights reserved.

Redistribution and use in source and binary forms, with or without

modification, are permitted provided that the following conditions are met:

* Redistributions of source code must retain the above copyright notice, this

list of conditions and the following disclaimer.

* Redistributions in binary form must reproduce the above copyright notice,

this list of conditions and the following disclaimer in the documentation

and/or other materials provided with the distribution.

* Neither the name of tushare nor the names of its

contributors may be used to endorse or promote products derived from

this software without specific prior written permission.

THIS SOFTWARE IS PROVIDED BY THE COPYRIGHT HOLDERS AND CONTRIBUTORS "AS IS"

AND ANY EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, THE

IMPLIED WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE ARE

DISCLAIMED. IN NO EVENT SHALL THE COPYRIGHT HOLDER OR CONTRIBUTORS BE LIABLE

FOR ANY DIRECT, INDIRECT, INCIDENTAL, SPECIAL, EXEMPLARY, OR CONSEQUENTIAL

DAMAGES (INCLUDING, BUT NOT LIMITED TO, PROCUREMENT OF SUBSTITUTE GOODS OR

SERVICES; LOSS OF USE, DATA, OR PROFITS; OR BUSINESS INTERRUPTION) HOWEVER

CAUSED AND ON ANY THEORY OF LIABILITY, WHETHER IN CONTRACT, STRICT LIABILITY,

OR TORT (INCLUDING NEGLIGENCE OR OTHERWISE) ARISING IN ANY WAY OUT OF THE USE

OF THIS SOFTWARE, EVEN IF ADVISED OF THE POSSIBILITY OF SUCH DAMAGE.

================================================

FILE: MANIFEST

================================================

# file GENERATED by distutils, do NOT edit

setup.py

test\test.py

tushare\__init__.py

tushare\data\__init__.py

tushare\data\all.csv

tushare\stock\__init__.py

tushare\stock\cons.py

tushare\stock\fundamental.py

tushare\stock\trading.py

================================================

FILE: README.md

================================================

TuShare

Tushare Pro版已发布,请访问新的官网了解和查询数据接口! [https://tushare.pro](https://tushare.pro)

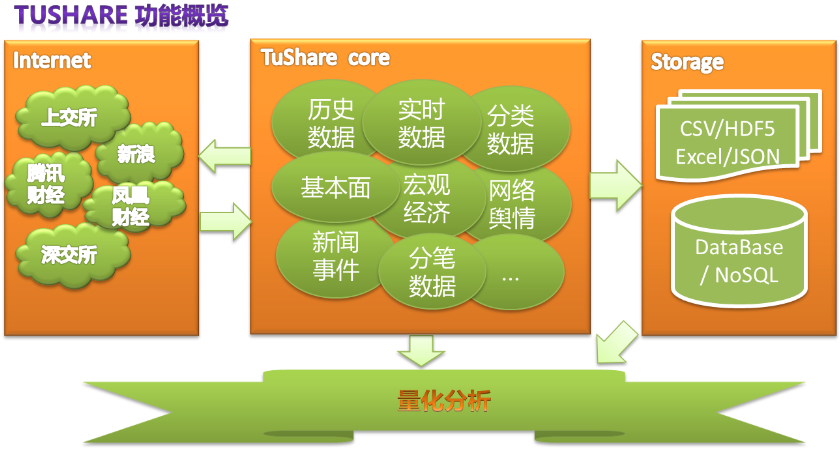

TuShare是实现对股票/期货等金融数据从**数据采集**、**清洗加工** 到 **数据存储**过程的工具,满足金融量化分析师和学习数据分析的人在数据获取方面的需求,它的特点是数据覆盖范围广,接口调用简单,响应快速。

欢迎关注扫描TuShare的微信公众号“挖地兔”,更多资源和信息与您分享。另外,由于tushare官网在重新设计和开发,最新接口的使用文档都会在挖地兔公众号发布,所以,请扫码关注,谢谢!

QQ交流群:

- 一群(已满):14934432

- 二群(付费高级用户群,可获得更多支持及参与圈子活动):658562506

- 三群(免费):665480579

- 四群 (免费) :527416821

Dependencies

=========

python 2.x/3.x

[pandas](http://pandas.pydata.org/ "pandas")

Installation

====

- 方式1:pip install tushare

- 方式2:python setup.py install

- 方式3:访问[https://pypi.python.org/pypi/tushare/](https://pypi.python.org/pypi/tushare/)下载安装

Upgrade

=======

pip install tushare --upgrade

Quick Start

======

**Example 1.** 获取个股历史交易数据(包括均线数据):

import tushare as ts

ts.get_hist_data('600848') #一次性获取全部数据

另外,参考get_k_data函数

结果显示:

> 日期 ,开盘价, 最高价, 收盘价, 最低价, 成交量, 价格变动 ,涨跌幅,5日均价,10日均价,20日均价,5日均量,10日均量,20日均量,换手率

open high close low volume p_change ma5 \

date

2012-01-11 6.880 7.380 7.060 6.880 14129.96 2.62 7.060

2012-01-12 7.050 7.100 6.980 6.900 7895.19 -1.13 7.020

2012-01-13 6.950 7.000 6.700 6.690 6611.87 -4.01 6.913

2012-01-16 6.680 6.750 6.510 6.480 2941.63 -2.84 6.813

2012-01-17 6.660 6.880 6.860 6.460 8642.57 5.38 6.822

2012-01-18 7.000 7.300 6.890 6.880 13075.40 0.44 6.788

2012-01-19 6.690 6.950 6.890 6.680 6117.32 0.00 6.770

2012-01-20 6.870 7.080 7.010 6.870 6813.09 1.74 6.832

ma10 ma20 v_ma5 v_ma10 v_ma20 turnover

date

2012-01-11 7.060 7.060 14129.96 14129.96 14129.96 0.48

2012-01-12 7.020 7.020 11012.58 11012.58 11012.58 0.27

2012-01-13 6.913 6.913 9545.67 9545.67 9545.67 0.23

2012-01-16 6.813 6.813 7894.66 7894.66 7894.66 0.10

2012-01-17 6.822 6.822 8044.24 8044.24 8044.24 0.30

2012-01-18 6.833 6.833 7833.33 8882.77 8882.77 0.45

2012-01-19 6.841 6.841 7477.76 8487.71 8487.71 0.21

2012-01-20 6.863 6.863 7518.00 8278.38 8278.38 0.23

设定历史数据的时间:

ts.get_hist_data('600848',start='2015-01-05',end='2015-01-09')

open high close low volume p_change ma5 ma10 \

date

2015-01-05 11.160 11.390 11.260 10.890 46383.57 1.26 11.156 11.212

2015-01-06 11.130 11.660 11.610 11.030 59199.93 3.11 11.182 11.155

2015-01-07 11.580 11.990 11.920 11.480 86681.38 2.67 11.366 11.251

2015-01-08 11.700 11.920 11.670 11.640 56845.71 -2.10 11.516 11.349

2015-01-09 11.680 11.710 11.230 11.190 44851.56 -3.77 11.538 11.363

ma20 v_ma5 v_ma10 v_ma20 turnover

date

2015-01-05 11.198 58648.75 68429.87 97141.81 1.59

2015-01-06 11.382 54854.38 63401.05 98686.98 2.03

2015-01-07 11.543 55049.74 61628.07 103010.58 2.97

2015-01-08 11.647 57268.99 61376.00 105823.50 1.95

2015-01-09 11.682 58792.43 60665.93 107924.27 1.54

**复权历史数据**

获取历史复权数据,分为前复权和后复权数据,接口提供股票上市以来所有历史数据,默认为前复权。如果不设定开始和结束日期,则返回近一年的复权数据,从性能上考虑,推荐设定开始日期和结束日期,而且最好不要超过一年以上,获取到数据后,请及时在本地存储。

ts.get_h_data('002337') #前复权

ts.get_h_data('002337',autype='hfq') #后复权

ts.get_h_data('002337',autype=None) #不复权

ts.get_h_data('002337',start='2015-01-01',end='2015-03-16') #两个日期之间的前复权数据

**Example 2.** 一次性获取最近一个日交易日所有股票的交易数据(结果显示速度取决于网速)

ts.get_today_all()

结果显示:

> 代码,名称,涨跌幅,现价,开盘价,最高价,最低价,最日收盘价,成交量,换手率

code name changepercent trade open high low settlement \

0 002738 中矿资源 10.023 19.32 19.32 19.32 19.32 17.56

1 300410 正业科技 10.022 25.03 25.03 25.03 25.03 22.75

2 002736 国信证券 10.013 16.37 16.37 16.37 16.37 14.88

3 300412 迦南科技 10.010 31.54 31.54 31.54 31.54 28.67

4 300411 金盾股份 10.007 29.68 29.68 29.68 29.68 26.98

5 603636 南威软件 10.006 38.15 38.15 38.15 38.15 34.68

6 002664 信质电机 10.004 30.68 29.00 30.68 28.30 27.89

7 300367 东方网力 10.004 86.76 78.00 86.76 77.87 78.87

8 601299 中国北车 10.000 11.44 11.44 11.44 11.29 10.40

9 601880 大连港 10.000 5.72 5.34 5.72 5.22 5.20

10 000856 冀东装备 10.000 8.91 8.18 8.91 8.18 8.10

volume turnoverratio

0 375100 1.25033

1 85800 0.57200

2 1058925 0.08824

3 69400 0.51791

4 252220 1.26110

5 1374630 5.49852

6 6448748 9.32700

7 2025030 6.88669

8 433453523 4.28056

9 323469835 9.61735

10 25768152 19.51090

**Example 3.** 获取历史分笔数据

import tushare as ts

df = ts.get_tick_data('600848',date='2014-01-09')

df.head(10)

结果显示:

>成交时间、成交价格、价格变动,成交手、成交金额(元),买卖类型

Out[3]:

time price change volume amount type

0 15:00:00 6.05 -- 8 4840 卖盘

1 14:59:55 6.05 -- 50 30250 卖盘

2 14:59:35 6.05 -- 20 12100 卖盘

3 14:59:30 6.05 -0.01 165 99825 卖盘

4 14:59:20 6.06 0.01 4 2424 买盘

5 14:59:05 6.05 -0.01 2 1210 卖盘

6 14:58:55 6.06 -- 4 2424 买盘

7 14:58:45 6.06 -- 2 1212 买盘

8 14:58:35 6.06 0.01 2 1212 买盘

9 14:58:25 6.05 -0.01 20 12100 卖盘

10 14:58:05 6.06 -- 5 3030 买盘

**Example 4.** 获取实时交易数据(Realtime Quotes Data)

df = ts.get_realtime_quotes('000581') #Single stock symbol

df[['code','name','price','bid','ask','volume','amount','time']]

结果显示:

>名称、开盘价、昨价、现价、最高、最低、买入价、卖出价、成交量、成交金额...more in docs

code name price bid ask volume amount time

0 000581 威孚高科 31.15 31.14 31.15 8183020 253494991.16 11:30:36

请求多个股票方法(一次最好不要超过30个):

ts.get_realtime_quotes(['600848','000980','000981']) #symbols from a list

ts.get_realtime_quotes(df['code'].tail(10)) #from a Series

更多文档

========

[https://tushare.pro](https://tushare.pro)

[http://tushare.org/](http://tushare.org/ "TuShare Docs")

Change Logs

-----------

1.2.17 2018/11/24

======

- Pro版增加期货数据

- Pro版增加A股周/月数据

- Pro版增加通用行情pro_bar接口股票/基金/期货/数据货币行情的支持,同时支持股票的复权行情

1.2.15 2018/10/15

====

- 增加通用行情pro_bar接口

- 优化set_token功能

1.2.12 2018/08/10

====

- 发布Pro版第一稿

- 发布Pro网站,[https://tushare.pro](https://tushare.pro)

1.0.5 2017/11/12

======

- 新增可转债数据

- 增加长连接关闭函数

- 修复部分bug

1.0.2 2017/10/29

==========

- 新增bar接口,支持更稳定的股票、ETF、期货期权、港股、中概股等品种

- 新增tick接口,支持以上品种的成交数据

- 新增沪深港通每日资金流向数据

- 修复了部分bug

0.9.2 2017/09/13

===========

- 新增数据货币行情数据接口,同时支持火币、okcoin、中国比特币

- 部分bug修复

0.8.8 2017/08/29

===========

- 新增分红送股数据(包含历史)

- 新增get_day_all接口

- 新增BDI接口

0.8.0 2017/06/05

===========

- 新增期货行情数据6个接口,感谢debugo贡献代码

- 修复部分bug

0.7.6 2017/05/16

=============

- get\_today\_all接口数据补齐

- forecast\_data mac下编码问题修复

0.7.0 2017/03/12

=============

- get\_today\_all接口提速

- 版本累积更新

0.6.2 2016/12/03

==========

- 新增十大股东和十大流通股接口 top10_holders

- 新增全球实时指数列表接口 global_realtime

- 修复部分bug

0.6.1 2016/11/22

===========

- 修正get_k_databug

- 修正实盘交易登录问题

0.5.6 2016/11/06

=============

- 新增全新行情数据接口get_k_data(请关注tushare公众号“挖地兔”后查看历史文章《全新的免费行情数据接口》)

- 修复程序和文档bug

0.5.1 2016/10/16

=============

- 新增实盘交易接口

- 修复bug

0.4.9 2016/03/26

=============

- 新增申万行业分类get_industry_classified(standard='sw')

- 新增交易日历trade_cal()

- 修复bug

0.4.3 2015/12/24

============

- 新增电影票房数据

- 修复部分bug

0.4.1 2015/11/27

==============

- 新增sina大单数据

- 修改当日分笔bug

- 深市融资融券数据修复

0.3.9 2015/10/13

============

- 新增期权隐含波动率数据

- 修复指数成份及权重接口问题

0.3.8 2015/09/19

============

- 沪深300成份股和权重接口问题修复

- 其它bug的修复

0.3.5 2015/07/27

==========

- 部分代码修正

0.3.4 2015/06/15

===========

- 新增‘龙虎榜’模块

1. 每日龙虎榜列表

1. 个股上榜统计

1. 营业部上榜统计

1. 龙虎榜机构席位追踪

1. 龙虎榜机构席位成交明细

- 修改get\_h\_data数据类型为float

- 修改get_index接口遗漏的open列

- 合并GitHub上提交的bug修复

0.2.8 2015/04/28

============

- 新增大盘指数实时行情列表

- 新增大盘指数历史行情数据(全部)

- 新增终止上市公司列表(退市)

- 新增暂停上市公司列表

- 修正融资融券明细无日期的缺陷

- 修正get\_h\_data部分bug

0.2.6

========

- 新增沪市融资融券列表

- 新增沪市融资融券明细列表

- 新增深市融资融券列表

- 新增深市融资融券明细列表

- 修正复权数据数据源出现null造成异常问题(对大约300个股票有影响)

0.2.5 2015/04/16

===========

- 完成python2.x和python3.x兼容性支持

- 部分算法优化和代码重构

- 新增中证500成份股

- 新增当日分笔交易明细

- 修正分配预案(高送转)bug

0.2.3 2015/04/11

===========

- 新增“新浪股吧”消息和热度

- 新增新股上市数据

- 修正“基本面”模块中数据重复的问题

- 修正历史数据缺少一列column(数据来源问题)的bug

0.2.0 2015/03/17

=======

- 新增历史复权数据接口

- 新增即时滚动新闻、信息地雷数据

- 新增沪深300指数成股份及动态权重、

- 新增上证50指数成份股

- 修改历史行情数据类型为float

0.1.9 2015/02/06

========

- 增加分类数据

- 增加数据存储示例

0.1.6 2015/01/27

========

- 增加了重点指数的历史和实时行情

- 更新docs

0.1.5 2015/01/26

=====

- 增加基本面数据接口

- 发布一版使用手册,开通[TuShare docs](http://tushare.waditu.com)网站

0.1.3 2015/01/13

===

- 增加实时交易数据的获取

- Done for crawling Realtime Quotes data

0.1.1 2015/01/11

===

- 增加tick数据的获取

0.1.0 2014/12/01

===

- 创建第一个版本

- 实现个股历史数据的获取

================================================

FILE: issues/from_email.txt

================================================

2015-2-10

------------

ASK:Stupidinsect:ϣӻ

REP:

2015-2-26

------------

ASK:Allisnoneproblem with python keywords

REP:н

2015-3-1

------------

ASK:: get_hist_dataMySQLdate(index)

REP:ʱͨdf['date'] = df.indexto_sqlòindex=Falseһ汾ȡindex

2015-3-23

--------------

chendonghui1987:ȡǰȨݱTypeError: cannot convert the series to <type 'float'>

from v0.2.1

2015-04-05

-------------------

̹:

JimmyTuã

ȸлṩôõһ⣬Һܾõ⣬

ύһbugع˾걨ݣreport = ts.get_report_data(2014, 1)

⣺

1ȱ˾ƽУ000001

2˾ظ總ˢ

ϣлָ

2015-04-18

---------------

huhaook:ijЩɵĸȨ쳣ʵԴΪnullҪij(418)

2015-04-28

----------------

Ԭͨget_hist_dataȡ600102ʱ600102йƱݷأֱӷNone

2015-06-13

Tales Yuantushareprofit_dataȡ2015Ԥʧܡ61423ʱ25

================================================

FILE: issues/from_sns.txt

================================================

2015-02-12

-----------

QQȺ297882961kݸȨ۵⡢ݲ

2015-03-01

-----------

QQȺ275882700@ kߴ⣬ȷʵǷ˲ƾԴ⣨ɸget_h_data()ӿڣ

2015-03-02

-----------

QQȺ275882700@װ˹̹ ϣṩָijɷݹɺȨ

2015-03-20

QQȺ297882961:@x ֤100֤800ָk

2015-04-09

-------------

QQȺ297882961:@㽭-QT002738Ʊʷݱget_hist_data飬ԭǷ˲ƾĽӿһлʵݡʽжһcolumnsöԵȵcolumsб

2015-04-10

-------------

־ȨݵΪobject

2015-04-16

-------------

@ariestigerget_h_data()ijɽƴд

2015-05-01

------------------

QQȺ297882961:@Koffʹget_today_tickӿڵʱUnboundLocalError: local variable 'data' referenced before assignment쳣̺ϵõģ

2015-05-05

QQ Mr.OKӹ˾ɶĽӿ

PHENXI-ڻ

--------------------

http://vip.stock.finance.sina.com.cn/mkt/#hqIndex

ҳбȽȫгϢ

http://blog.sina.com.cn/s/blog_7ed3ed3d0101gphj.html

ƪгһЩݽṹ

http://quote.hexun.com/futures/newfutures.aspx?market=9&type=all&n=%C8%AB%B2%BF

http://webcffex.hermes.hexun.com/cffex/kline?code=CFFEXIH1606&start=20160206091500&number=-1000&type=5

PHENXI 2016/2/15 8:57:44

http://webftcn.hermes.hexun.com/

http://webcffex.hermes.hexun.com/cffex/quotelist?code=CFFEXIH1606,CFFEXIF1609,CFFEXIC1603,dceA1611,CFFEXIC1512,&column=code,name,price,priceweight,updownrate,high,low,updown,lastclose,open&callback=getdata1&callback=jQuery111107492109271895186_1455497884413&_=1455497884414

================================================

FILE: requirements.txt

================================================

pandas>=0.18.0

requests>=2.0.0

lxml>=3.8.0

simplejson>=3.16.0

bs4>=0.0.1

beautfulsoup4>=4.5.1

================================================

FILE: setup.py

================================================

from setuptools import setup, find_packages

import codecs

import os

def read(fname):

return codecs.open(os.path.join(os.path.dirname(__file__), fname)).read()

long_desc = """

TuShare

===============

.. image:: https://api.travis-ci.org/waditu/tushare.png?branch=master

:target: https://travis-ci.org/waditu/tushare

.. image:: https://badge.fury.io/py/tushare.png

:target: http://badge.fury.io/py/tushare

* easy to use as most of the data returned are pandas DataFrame objects

* can be easily saved as csv, excel or json files

* can be inserted into MySQL or Mongodb

Target Users

--------------

* financial market analyst of China

* learners of financial data analysis with pandas/NumPy

* people who are interested in China financial data

Installation

--------------

pip install tushare

Upgrade

---------------

pip install tushare --upgrade

Quick Start

--------------

::

import tushare as ts

ts.get_hist_data('600848')

return::

open high close low volume p_change ma5 \

date

2012-01-11 6.880 7.380 7.060 6.880 14129.96 2.62 7.060

2012-01-12 7.050 7.100 6.980 6.900 7895.19 -1.13 7.020

2012-01-13 6.950 7.000 6.700 6.690 6611.87 -4.01 6.913

2012-01-16 6.680 6.750 6.510 6.480 2941.63 -2.84 6.813

2012-01-17 6.660 6.880 6.860 6.460 8642.57 5.38 6.822

2012-01-18 7.000 7.300 6.890 6.880 13075.40 0.44 6.788

2012-01-19 6.690 6.950 6.890 6.680 6117.32 0.00 6.770

2012-01-20 6.870 7.080 7.010 6.870 6813.09 1.74 6.832

"""

def read_install_requires():

reqs = [

'pandas>=0.18.0',

'requests>=2.0.0',

'lxml>=3.8.0',

'simplejson>=3.16.0',

'msgpack>=0.5.6',

'pyzmq>=16.0.0'

]

return reqs

setup(

name='tushare',

version=read('tushare/VERSION.txt'),

description='A utility for crawling historical and Real-time Quotes data of China stocks',

# long_description=read("READM.rst"),

long_description = long_desc,

author='Jimmy Liu',

author_email='jimmysoa@sina.cn',

license='BSD',

url='http://tushare.org',

install_requires=read_install_requires(),

keywords='Global Financial Data',

classifiers=['Development Status :: 4 - Beta',

'Programming Language :: Python :: 2.6',

'Programming Language :: Python :: 2.7',

'Programming Language :: Python :: 3.2',

'Programming Language :: Python :: 3.3',

'Programming Language :: Python :: 3.4',

'Programming Language :: Python :: 3.5',

'License :: OSI Approved :: BSD License'],

packages=find_packages(),

include_package_data=True,

package_data={'': ['*.csv', '*.txt']},

)

================================================

FILE: test/__init__.py

================================================

================================================

FILE: test/bar_test.py

================================================

# -*- coding:utf-8 -*-

'''

Created on 2017/9/24

@author: Jimmy Liu

'''

import unittest

import tushare.stock.trading as fd

class Test(unittest.TestCase):

def set_data(self):

self.code = '600848'

self.start = ''

self.end = ''

def test_bar_data(self):

self.set_data()

print(fd.bar(self.code, self.start, self.end))

if __name__ == "__main__":

#import sys;sys.argv = ['', 'Test.testName']

unittest.main()

================================================

FILE: test/billboard_test.py

================================================

# -*- coding:utf-8 -*-

'''

Created on 2015/3/14

@author: Jimmy Liu

'''

import unittest

import tushare.stock.billboard as fd

class Test(unittest.TestCase):

def set_data(self):

self.date = '2015-06-12'

self.days = 5

def test_top_list(self):

self.set_data()

print(fd.top_list(self.date))

def test_cap_tops(self):

self.set_data()

print(fd.cap_tops(self.days))

def test_broker_tops(self):

self.set_data()

print(fd.broker_tops(self.days))

def test_inst_tops(self):

self.set_data()

print(fd.inst_tops(self.days))

def test_inst_detail(self):

print(fd.inst_detail())

if __name__ == "__main__":

unittest.main()

================================================

FILE: test/classifying_test.py

================================================

# -*- coding:utf-8 -*-

'''

Created on 2015/3/14

@author: Jimmy Liu

'''

import unittest

import tushare.stock.classifying as fd

class Test(unittest.TestCase):

def set_data(self):

self.code = '600848'

self.start = '2015-01-03'

self.end = '2015-04-07'

self.year = 2014

self.quarter = 4

def test_get_industry_classified(self):

print(fd.get_industry_classified())

def test_get_concept_classified(self):

print(fd.get_concept_classified())

def test_get_area_classified(self):

print(fd.get_area_classified())

def test_get_gem_classified(self):

print(fd.get_gem_classified())

def test_get_sme_classified(self):

print(fd.get_sme_classified())

def test_get_st_classified(self):

print(fd.get_st_classified())

def test_get_hs300s(self):

print(fd.get_hs300s())

def test_get_sz50s(self):

print(fd.get_sz50s())

def test_get_zz500s(self):

print(fd.get_zz500s())

if __name__ == "__main__":

unittest.main()

# suite = unittest.TestSuite()

# suite.addTest(Test('test_get_gem_classified'))

# unittest.TextTestRunner(verbosity=2).run(suite)

================================================

FILE: test/dateu_test.py

================================================

# -*- coding:utf-8 -*-

"""

@author: ZackZK

"""

from unittest import TestCase

from tushare.util import dateu

from tushare.util.dateu import is_holiday

class Test_Is_holiday(TestCase):

def test_is_holiday(self):

dateu.holiday = ['2016-01-04'] # holiday stub for later test

self.assertTrue(is_holiday('2016-01-04')) # holiday

self.assertFalse(is_holiday('2016-01-01')) # not holiday

self.assertTrue(is_holiday('2016-01-09')) # Saturday

self.assertTrue(is_holiday('2016-01-10')) # Sunday

================================================

FILE: test/fund_test.py

================================================

# -*- coding:utf-8 -*-

import unittest

import tushare.stock.fundamental as fd

class Test(unittest.TestCase):

def set_data(self):

self.code = '600848'

self.start = '2015-01-03'

self.end = '2015-04-07'

self.year = 2014

self.quarter = 4

def test_get_stock_basics(self):

print(fd.get_stock_basics())

# def test_get_report_data(self):

# self.set_data()

# print(fd.get_report_data(self.year, self.quarter))

#

# def test_get_profit_data(self):

# self.set_data()

# print(fd.get_profit_data(self.year, self.quarter))

#

# def test_get_operation_data(self):

# self.set_data()

# print(fd.get_operation_data(self.year, self.quarter))

#

# def test_get_growth_data(self):

# self.set_data()

# print(fd.get_growth_data(self.year, self.quarter))

#

# def test_get_debtpaying_data(self):

# self.set_data()

# print(fd.get_debtpaying_data(self.year, self.quarter))

#

# def test_get_cashflow_data(self):

# self.set_data()

# print(fd.get_cashflow_data(self.year, self.quarter))

if __name__ == '__main__':

unittest.main()

================================================

FILE: test/indictor_test.py

================================================

# -*- coding:utf-8 -*-

'''

Created on 2018/05/26

@author: Jackie Liao

'''

import unittest

import tushare.stock.indictor as idx

import tushare as ts

class Test(unittest.TestCase):

def test_plot_all(self):

data = ts.get_k_data("601398", start="2018-01-01", end="2018-05-27")

data = data.sort_values(by=["date"], ascending=True)

idx.plot_all(data, is_show=True, output=None)

if __name__ == "__main__":

# import sys;sys.argv = ['', 'Test.testName']

unittest.main()

================================================

FILE: test/macro_test.py

================================================

# -*- coding:utf-8 -*-

'''

Created on 2015/3/14

@author: Jimmy Liu

'''

import unittest

import tushare.stock.macro as fd

class Test(unittest.TestCase):

def test_get_gdp_year(self):

print(fd.get_gdp_year())

def test_get_gdp_quarter(self):

print(fd.get_gdp_quarter())

def test_get_gdp_for(self):

print(fd.get_gdp_for())

def test_get_gdp_pull(self):

print(fd.get_gdp_pull())

def test_get_gdp_contrib(self):

print(fd.get_gdp_contrib())

def test_get_cpi(self):

print(fd.get_cpi())

def test_get_ppi(self):

print(fd.get_ppi())

def test_get_deposit_rate(self):

print(fd.get_deposit_rate())

def test_get_loan_rate(self):

print(fd.get_loan_rate())

def test_get_rrr(self):

print(fd.get_rrr())

def test_get_money_supply(self):

print(fd.get_money_supply())

def test_get_money_supply_bal(self):

print(fd.get_money_supply_bal())

if __name__ == "__main__":

#import sys;sys.argv = ['', 'Test.testName']

unittest.main()

================================================

FILE: test/nav_test.py

================================================

# -*- coding:utf-8 -*-

'''

Created on 2016/5/26

@author: leo

'''

import unittest

import tushare.fund.nav as nav

class Test(unittest.TestCase):

def set_data(self):

self.symbol = '600848'

self.start = '2014-11-24'

self.end = '2016-02-29'

self.disp = 5

def test_get_nav_open(self):

self.set_data()

lst = ['all', 'equity', 'mix', 'bond', 'monetary', 'qdii']

print('get nav open................\n')

for item in lst:

print('=============\nget %s nav\n=============' % item)

fund_df = nav.get_nav_open(item)

print('\nnums=%d' % len(fund_df))

print(fund_df[:self.disp])

def test_get_nav_close(self):

self.set_data()

type2 = ['all', 'fbqy', 'fbzq']

qy_t3 = ['all', 'ct', 'cx']

zq_t3 = ['all', 'wj', 'jj', 'cz']

print('\nget nav closed................\n')

fund_df = None

for item in type2:

if item == 'fbqy':

for t3i in qy_t3:

print('\n=============\nget %s-%s nav\n=============' %

(item, t3i))

fund_df = nav.get_nav_close(item, t3i)

print('\nnums=%d' % len(fund_df))

print(fund_df[:self.disp])

elif item == 'fbzq':

for t3i in zq_t3:

print('\n=============\nget %s-%s nav\n=============' %

(item, t3i))

fund_df = nav.get_nav_close(item, t3i)

print('\nnums=%d' % len(fund_df))

print(fund_df[:self.disp])

else:

print('\n=============\nget %s nav\n=============' % item)

fund_df = nav.get_nav_close(item)

print('\nnums=%d' % len(fund_df))

print(fund_df[:self.disp])

def test_get_nav_grading(self):

self.set_data()

t2 = ['all', 'fjgs', 'fjgg']

t3 = {'all': '0', 'wjzq': '13', 'gp': '14',

'zs': '15', 'czzq': '16', 'jjzq': '17'}

print('\nget nav grading................\n')

fund_df = None

for item in t2:

if item == 'all':

print('\n=============\nget %s nav\n=============' % item)

fund_df = nav.get_nav_grading(item)

print('\nnums=%d' % len(fund_df))

print(fund_df[:self.disp])

else:

for t3i in t3.keys():

print('\n=============\nget %s-%s nav\n=============' %

(item, t3i))

fund_df = nav.get_nav_grading(item, t3i)

print('\nnums=%d' % len(fund_df))

print(fund_df[:self.disp])

def test_nav_history(self):

self.set_data()

lst = ['164905', '161005', '380007', '000733', '159920', '164902',

'184721', '165519', '164302', '519749', '150275', '150305',

'150248']

for _, item in enumerate(lst):

print('\n=============\nget %s nav\n=============' % item)

fund_df = nav.get_nav_history(item, self.start, self.end)

if fund_df is not None:

print('\nnums=%d' % len(fund_df))

print(fund_df[:self.disp])

def test_get_fund_info(self):

self.set_data()

lst = ['164905', '161005', '380007', '000733', '159920', '164902',

'184721', '165519', '164302', '519749', '150275', '150305',

'150248']

for item in lst:

print('\n=============\nget %s nav\n=============' % item)

fund_df = nav.get_fund_info(item)

if fund_df is not None:

print('%s fund info' % item)

print(fund_df)

if __name__ == '__main__':

unittest.main()

================================================

FILE: test/news_test.py

================================================

# -*- coding:utf-8 -*-

'''

Created on 2015/3/14

@author: Jimmy Liu

'''

import unittest

import tushare.stock.newsevent as fd

class Test(unittest.TestCase):

def set_data(self):

self.code = '600848'

self.start = '2015-01-03'

self.end = '2015-04-07'

self.year = 2014

self.quarter = 4

self.top = 60

self.show_content = True

def test_get_latest_news(self):

self.set_data()

print(fd.get_latest_news(self.top, self.show_content))

def test_get_notices(self):

self.set_data()

df = fd.get_notices(self.code)

print(fd.notice_content(df.ix[0]['url']))

def test_guba_sina(self):

self.set_data()

print(fd.guba_sina(self.show_content))

if __name__ == "__main__":

unittest.main()

================================================

FILE: test/ref_test.py

================================================

# -*- coding:utf-8 -*-

'''

Created on 2015/3/14

@author: Jimmy Liu

'''

import unittest

from tushare.stock import reference as fd

class Test(unittest.TestCase):

def set_data(self):

self.code = '600848'

self.start = '2015-01-03'

self.end = '2015-04-07'

self.year = 2014

self.quarter = 4

self.top = 60

self.show_content = True

def test_profit_data(self):

self.set_data()

print(fd.profit_data(top=self.top))

def test_forecast_data(self):

self.set_data()

print(fd.forecast_data(self.year, self.quarter))

def test_xsg_data(self):

print(fd.xsg_data())

def test_fund_holdings(self):

self.set_data()

print(fd.fund_holdings(self.year, self.quarter))

def test_new_stocksa(self):

print(fd.new_stocks())

def test_sh_margin_details(self):

self.set_data()

print(fd.sh_margin_details(self.start, self.end, self.code))

def test_sh_margins(self):

self.set_data()

print(fd.sh_margins(self.start, self.end))

def test_sz_margins(self):

self.set_data()

print(fd.sz_margins(self.start, self.end))

def test_sz_margin_details(self):

self.set_data()

print(fd.sz_margin_details(self.end))

if __name__ == "__main__":

unittest.main()

================================================

FILE: test/shibor_test.py

================================================

# -*- coding:utf-8 -*-

import unittest

import tushare.stock.shibor as fd

class Test(unittest.TestCase):

def set_data(self):

self.year = 2014

# self.year = None

def test_shibor_data(self):

self.set_data()

fd.shibor_data(self.year)

def test_shibor_quote_data(self):

self.set_data()

fd.shibor_quote_data(self.year)

def test_shibor_ma_data(self):

self.set_data()

fd.shibor_ma_data(self.year)

def test_lpr_data(self):

self.set_data()

fd.lpr_data(self.year)

def test_lpr_ma_data(self):

self.set_data()

fd.lpr_ma_data(self.year)

if __name__ == '__main__':

unittest.main()

================================================

FILE: test/storing_test.py

================================================

# -*- coding:utf-8 -*-

import os

from sqlalchemy import create_engine

from pandas.io.pytables import HDFStore

import tushare as ts

def csv():

df = ts.get_hist_data('000875')

df.to_csv('c:/day/000875.csv',columns=['open','high','low','close'])

def xls():

df = ts.get_hist_data('000875')

#直接保存

df.to_excel('c:/day/000875.xlsx', startrow=2,startcol=5)

def hdf():

df = ts.get_hist_data('000875')

# df.to_hdf('c:/day/store.h5','table')

store = HDFStore('c:/day/store.h5')

store['000875'] = df

store.close()

def json():

df = ts.get_hist_data('000875')

df.to_json('c:/day/000875.json',orient='records')

#或者直接使用

print(df.to_json(orient='records'))

def appends():

filename = 'c:/day/bigfile.csv'

for code in ['000875', '600848', '000981']:

df = ts.get_hist_data(code)

if os.path.exists(filename):

df.to_csv(filename, mode='a', header=None)

else:

df.to_csv(filename)

def db():

df = ts.get_tick_data('600848',date='2014-12-22')

engine = create_engine('mysql://root:jimmy1@127.0.0.1/mystock?charset=utf8')

# db = MySQLdb.connect(host='127.0.0.1',user='root',passwd='jimmy1',db="mystock",charset="utf8")

# df.to_sql('TICK_DATA',con=db,flavor='mysql')

# db.close()

df.to_sql('tick_data',engine,if_exists='append')

def nosql():

import pymongo

import json

conn = pymongo.Connection('127.0.0.1', port=27017)

df = ts.get_tick_data('600848',date='2014-12-22')

print(df.to_json(orient='records'))

conn.db.tickdata.insert(json.loads(df.to_json(orient='records')))

# print conn.db.tickdata.find()

if __name__ == '__main__':

nosql()

================================================

FILE: test/trading_test.py

================================================

# -*- coding:utf-8 -*-

'''

Created on 2015/3/14

@author: Jimmy Liu

'''

import unittest

import tushare.stock.trading as fd

class Test(unittest.TestCase):

def set_data(self):

self.code = '600848'

self.start = '2015-01-03'

self.end = '2015-04-07'

self.year = 2014

self.quarter = 4

def test_get_hist_data(self):

self.set_data()

print(fd.get_hist_data(self.code, self.start))

def test_get_tick_data(self):

self.set_data()

print(fd.get_tick_data(self.code, self.end))

def test_get_today_all(self):

print(fd.get_today_all())

def test_get_realtime_quotesa(self):

self.set_data()

print(fd.get_realtime_quotes(self.code))

def test_get_h_data(self):

self.set_data()

print(fd.get_h_data(self.code, self.start, self.end))

def test_get_today_ticks(self):

self.set_data()

print(fd.get_today_ticks(self.code))

if __name__ == "__main__":

#import sys;sys.argv = ['', 'Test.testName']

unittest.main()

================================================

FILE: test_unittest.py

================================================

'''

UnitTest for API

@author: Jimmy

'''

import unittest

import tushare.stock.trading as td

class TestTrading(unittest.TestCase):

def set_data(self):

self.code = '600848'

self.start = '2014-11-03'

self.end = '2014-11-07'

def test_tickData(self):

self.set_data()

td.get_tick_data(self.code, date=self.start)

# def test_histData(self):

# self.set_data()

# td.get_hist_data(self.code, start=self.start, end=self.end)

if __name__ == "__main__":

#import sys;sys.argv = ['', 'Test.testName']

unittest.main()

================================================

FILE: tushare/VERSION.txt

================================================

1.2.18

================================================

FILE: tushare/__init__.py

================================================

# -*- coding:utf-8 -*-

import codecs

import os

__version__ = codecs.open(os.path.join(os.path.dirname(__file__), 'VERSION.txt')).read()

__author__ = 'Jimmy Liu'

"""

for trading data

"""

from tushare.stock.trading import (get_hist_data, get_tick_data,

get_today_all, get_realtime_quotes,

get_h_data, get_today_ticks,

get_index, get_hists,

get_k_data, get_day_all,

get_sina_dd, bar, tick,

get_markets, quotes,

get_instrument, reset_instrument)

"""

for trading data

"""

from tushare.stock.fundamental import (get_stock_basics, get_report_data,

get_profit_data,

get_operation_data, get_growth_data,

get_debtpaying_data, get_cashflow_data,

get_balance_sheet, get_profit_statement, get_cash_flow)

"""

for macro data

"""

from tushare.stock.macro import (get_gdp_year, get_gdp_quarter,

get_gdp_for, get_gdp_pull,

get_gdp_contrib, get_cpi,

get_ppi, get_deposit_rate,

get_loan_rate, get_rrr,

get_money_supply, get_money_supply_bal,

get_gold_and_foreign_reserves)

"""

for classifying data

"""

from tushare.stock.classifying import (get_industry_classified, get_concept_classified,

get_area_classified, get_gem_classified,

get_sme_classified, get_st_classified,

get_hs300s, get_sz50s, get_zz500s,

get_terminated, get_suspended)

"""

for macro data

"""

from tushare.stock.newsevent import (get_latest_news, latest_content,

get_notices, notice_content,

guba_sina)

"""

for reference

moneyflow_hsgt:沪深港通资金流向

"""

from tushare.stock.reference import (profit_data, forecast_data,

xsg_data, fund_holdings,

new_stocks, new_cbonds, sh_margins,

sh_margin_details,

sz_margins, sz_margin_details,

top10_holders, profit_divis,

moneyflow_hsgt, margin_detail,

margin_target, margin_offset,

margin_zsl, stock_issuance,

stock_pledged, pledged_detail)

"""

for shibor

"""

from tushare.stock.shibor import (shibor_data, shibor_quote_data,

shibor_ma_data, lpr_data,

lpr_ma_data)

"""

for tushare pro api

"""

from tushare.pro.data_pro import (pro_api, pro_bar)

"""

for LHB

"""

from tushare.stock.billboard import (top_list, cap_tops, broker_tops,

inst_tops, inst_detail)

"""

for utils

"""

from tushare.util.dateu import (trade_cal, is_holiday)

from tushare.internet.boxoffice import (realtime_boxoffice, day_boxoffice,

day_cinema, month_boxoffice)

from tushare.internet.indexes import (bdi)

"""

for fund data

"""

from tushare.fund.nav import (get_nav_open, get_nav_close, get_nav_grading,

get_nav_history, get_fund_info)

"""

for trader API

"""

from tushare.trader.trader import TraderAPI

"""

for futures API

"""

from tushare.futures.intlfutures import (get_intlfuture)

from tushare.stock.globals import (global_realtime)

from tushare.util.mailmerge import (MailMerge)

"""

for futures API

"""

from tushare.futures.domestic import (get_cffex_daily, get_czce_daily,

get_dce_daily, get_future_daily,

get_shfe_daily, get_shfe_vwap)

from tushare.coins.market import (coins_tick, coins_bar,

coins_snapshot, coins_trade)

from tushare.util.conns import (get_apis, close_apis)

from tushare.util.upass import (get_token, set_token)

================================================

FILE: tushare/bond/__init__.py

================================================

================================================

FILE: tushare/bond/bonds.py

================================================

# -*- coding:utf-8 -*-

"""

投资参考数据接口

Created on 2017/10/01

@author: Jimmy Liu

@group : waditu

@contact: jimmysoa@sina.cn

"""

def get_bond_info(code):

pass

if __name__ == '__main__':

pass

================================================

FILE: tushare/coins/__init__.py

================================================

================================================

FILE: tushare/coins/market.py

================================================

#!/usr/bin/env python

# -*- coding:utf-8 -*-

"""

数字货币行情数据

Created on 2017年9月9日

@author: Jimmy Liu

@group : waditu

@contact: jimmysoa@sina.cn

"""

import pandas as pd

import traceback

import time

import json

try:

from urllib.request import urlopen, Request

except ImportError:

from urllib2 import urlopen, Request

URL = {

"hb": {

"rt" : 'http://api.huobi.com/staticmarket/ticker_%s_json.js',

"kline" : 'http://api.huobi.com/staticmarket/%s_kline_%s_json.js?length=%s',

"snapshot" : 'http://api.huobi.com/staticmarket/depth_%s_%s.js',

"tick" : 'http://api.huobi.com/staticmarket/detail_%s_json.js',

},

"ok": {

"rt" : 'https://www.okcoin.cn/api/v1/ticker.do?symbol=%s_cny',

"kline" : 'https://www.okcoin.cn/api/v1/kline.do?symbol=%s_cny&type=%s&size=%s',

"snapshot" : 'https://www.okcoin.cn/api/v1/depth.do?symbol=%s_cny&merge=&size=%s',

"tick" : 'https://www.okcoin.cn/api/v1/trades.do?symbol=%s_cny',

},

'chbtc': {

"rt" : 'http://api.chbtc.com/data/v1/ticker?currency=%s_cny',

"kline" : 'http://api.chbtc.com/data/v1/kline?currency=%s_cny&type=%s&size=%s',

"snapshot" : 'http://api.chbtc.com/data/v1/depth?currency=%s_cny&size=%s&merge=',

"tick" : 'http://api.chbtc.com/data/v1/trades?currency=%s_cny',

}

}

KTYPES = {

"D": {

"hb" : '100',

'ok' : '1day',

'chbtc' : '1day',

},

"W": {

"hb" : '200',

'ok' : '1week',

'chbtc' : '1week',

},

"M": {

"hb" : '300',

"ok" : '',

"chbtc" : '',

},

"1MIN": {

"hb" : '001',

'ok' : '1min',

'chbtc' : '1min',

},

"5MIN": {

"hb" : '005',

'ok' : '5min',

'chbtc' : '5min',

},

"15MIN": {

"hb" : '015',

'ok' : '15min',

'chbtc' : '15min',

},

"30MIN": {

"hb" : '030',

'ok' : '30min',

'chbtc' : '30min',

},

"60MIN": {

"hb" : '060',

'ok' : '1hour',

'chbtc' : '1hour',

},

}

def coins_tick(broker='hb', code='btc'):

"""

实时tick行情

params:

---------------

broker: hb:火币

ok:okCoin

chbtc:中国比特币

code: hb:btc,ltc

----okcoin---

btc_cny:比特币 ltc_cny:莱特币 eth_cny :以太坊 etc_cny :以太经典 bcc_cny :比特现金

----chbtc----

btc_cny:BTC/CNY

ltc_cny :LTC/CNY

eth_cny :以太币/CNY

etc_cny :ETC币/CNY

bts_cny :BTS币/CNY

eos_cny :EOS币/CNY

bcc_cny :BCC币/CNY

qtum_cny :量子链/CNY

hsr_cny :HSR币/CNY

return:json

---------------

hb:

{

"time":"1504713534",

"ticker":{

"symbol":"btccny",

"open":26010.90,

"last":28789.00,

"low":26000.00,

"high":28810.00,

"vol":17426.2198,

"buy":28750.000000,

"sell":28789.000000

}

}

ok:

{

"date":"1504713864",

"ticker":{

"buy":"28743.0",

"high":"28886.99",

"last":"28743.0",

"low":"26040.0",

"sell":"28745.0",

"vol":"20767.734"

}

}

chbtc:

{

u'date': u'1504794151878',

u'ticker': {

u'sell': u'28859.56',

u'buy': u'28822.89',

u'last': u'28859.56',

u'vol': u'2702.71',

u'high': u'29132',

u'low': u'27929'

}

}

"""

return _get_data(URL[broker]['rt'] % (code))

def coins_bar(broker='hb', code='btc', ktype='D', size='2000'):

"""

获取各类k线数据

params:

broker:hb,ok,chbtc

code:btc,ltc,eth,etc,bcc

ktype:D,W,M,1min,5min,15min,30min,60min

size:<2000

return DataFrame: 日期时间,开盘价,最高价,最低价,收盘价,成交量

"""

try:

js = _get_data(URL[broker]['kline'] % (code, KTYPES[ktype.strip().upper()][broker], size))

if js is None:

return js

if broker == 'chbtc':

js = js['data']

df = pd.DataFrame(js, columns=['DATE', 'OPEN', 'HIGH', 'LOW', 'CLOSE', 'VOL'])

if broker == 'hb':

if ktype.strip().upper() in ['D', 'W', 'M']:

df['DATE'] = df['DATE'].apply(lambda x: x[0:8])

else:

df['DATE'] = df['DATE'].apply(lambda x: x[0:12])

else:

df['DATE'] = df['DATE'].apply(lambda x: int2time(x / 1000))

if ktype.strip().upper() in ['D', 'W', 'M']:

df['DATE'] = df['DATE'].apply(lambda x: str(x)[0:10])

df['DATE'] = pd.to_datetime(df['DATE'])

return df

except Exception:

print(traceback.print_exc())

def coins_snapshot(broker='hb', code='btc', size='5'):

"""

获取实时快照数据

params:

broker:hb,ok,chbtc

code:btc,ltc,eth,etc,bcc

size:<150

return Panel: asks,bids

"""

try:

js = _get_data(URL[broker]['snapshot'] % (code, size))

if js is None:

return js

if broker == 'hb':

timestr = js['ts']

timestr = int2time(timestr / 1000)

if broker == 'ok':

timestr = time.strftime("%Y-%m-%d %H:%M:%S", time.localtime())

if broker == 'chbtc':

timestr = js['timestamp']

timestr = int2time(timestr)

asks = pd.DataFrame(js['asks'], columns = ['price', 'vol'])

bids = pd.DataFrame(js['bids'], columns = ['price', 'vol'])

asks['time'] = timestr

bids['time'] = timestr

djs = {"asks": asks, "bids": bids}

pf = pd.Panel(djs)

return pf

except Exception:

print(traceback.print_exc())

def coins_trade(broker='hb', code='btc'):

"""

获取实时交易数据

params:

-------------

broker: hb,ok,chbtc

code:btc,ltc,eth,etc,bcc

return:

---------------

DataFrame

'tid':order id

'datetime', date time

'price' : trade price

'amount' : trade amount

'type' : buy or sell

"""

js = _get_data(URL[broker]['tick'] % code)

if js is None:

return js

if broker == 'hb':

df = pd.DataFrame(js['trades'])

df = df[['id', 'ts', 'price', 'amount', 'direction']]

df['ts'] = df['ts'].apply(lambda x: int2time(x / 1000))

if broker == 'ok':

df = pd.DataFrame(js)

df = df[['tid', 'date_ms', 'price', 'amount', 'type']]

df['date_ms'] = df['date_ms'].apply(lambda x: int2time(x / 1000))

if broker == 'chbtc':

df = pd.DataFrame(js)

df = df[['tid', 'date', 'price', 'amount', 'type']]

df['date'] = df['date'].apply(lambda x: int2time(x))

df.columns = ['tid', 'datetime', 'price', 'amount', 'type']

return df

def _get_data(url):

try:

request = Request(url)

lines = urlopen(request, timeout = 10).read()

if len(lines) < 50: #no data

return None

js = json.loads(lines.decode('GBK'))

return js

except Exception:

print(traceback.print_exc())

def int2time(timestamp):

value = time.localtime(timestamp)

dt = time.strftime('%Y-%m-%d %H:%M:%S', value)

return dt

================================================

FILE: tushare/data/__init__.py

================================================

__version__ = "0.0.1"

================================================

FILE: tushare/fund/__init__.py

================================================

================================================

FILE: tushare/fund/cons.py

================================================

# -*- coding:utf-8 -*-

"""

Created on 2016/04/03

@author: Leo

@group : lazytech

@contact: lazytech@sina.cn

"""

VERSION = '0.0.1'

P_TYPE = {'http': 'http://', 'ftp': 'ftp://'}

FORMAT = lambda x: '%.2f' % x

FORMAT4 = lambda x: '%.4f' % x

DOMAINS = {'sina': 'sina.com.cn', 'sinahq': 'sinajs.cn',

'ifeng': 'ifeng.com', 'sf': 'finance.sina.com.cn',

'ssf': 'stock.finance.sina.com.cn',

'vsf': 'vip.stock.finance.sina.com.cn',

'idx': 'www.csindex.com.cn', '163': 'money.163.com',

'em': 'eastmoney.com', 'sseq': 'query.sse.com.cn',

'sse': 'www.sse.com.cn', 'szse': 'www.szse.cn',

'oss': '218.244.146.57',

'shibor': 'www.shibor.org'}

NAV_OPEN_API = {'all': 'getNetValueOpen', 'equity': 'getNetValueOpen',

'mix': 'getNetValueOpen', 'bond': 'getNetValueOpen',

'monetary': 'getNetValueMoney', 'qdii': 'getNetValueOpen'}

NAV_OPEN_KEY = {'all': '6XxbX6h4CED0ATvW', 'equity': 'Gb3sH5uawH5WCUZ9',

'mix': '6XxbX6h4CED0ATvW', 'bond': 'Gb3sH5uawH5WCUZ9',

'monetary': 'uGo5qniFnmT5eQjp', 'qdii': 'pTYExKwRmqrSaP0P'}

NAV_OPEN_T2 = {'all': '0', 'equity': '2', 'mix': '1',

'bond': '3', 'monetary': '0', 'qdii': '6'}

NAV_OPEN_T3 = ''

NAV_CLOSE_API = 'getNetValueClose'

NAV_CLOSE_KEY = ''

NAV_CLOSE_T2 = {'all': '0', 'fbqy': '4', 'fbzq': '9'}

NAV_CLOSE_T3 = {'all': '0', 'ct': '10',

'cx': '11', 'wj': '3', 'jj': '5', 'cz': '12'}

NAV_GRADING_API = 'getNetValueCX'

NAV_GRADING_KEY = ''

NAV_GRADING_T2 = {'all': '0', 'fjgs': '7', 'fjgg': '8'}

NAV_GRADING_T3 = {'all': '0', 'wjzq': '13',

'gp': '14', 'zs': '15', 'czzq': '16', 'jjzq': '17'}

NAV_DEFAULT_PAGE = 1

##########################################################################

# 基金数据列名

NAV_OPEN_COLUMNS = ['symbol', 'sname', 'per_nav', 'total_nav', 'yesterday_nav',

'nav_rate', 'nav_a', 'nav_date', 'fund_manager',

'jjlx', 'jjzfe']

NAV_HIS_JJJZ = ['fbrq', 'jjjz', 'ljjz']

NAV_HIS_NHSY = ['fbrq', 'nhsyl', 'dwsy']

FUND_INFO_COLS = ['symbol', 'jjqc', 'jjjc', 'clrq', 'ssrq', 'xcr', 'ssdd',

'Type1Name', 'Type2Name', 'Type3Name', 'jjgm', 'jjfe',

'jjltfe', 'jjferq', 'quarter', 'glr', 'tgr']

NAV_CLOSE_COLUMNS = ['symbol', 'sname', 'per_nav', 'total_nav', 'nav_rate',

'discount_rate', 'nav_date', 'start_date', 'end_date',

'fund_manager', 'jjlx', 'jjzfe']

NAV_GRADING_COLUMNS = ['symbol', 'sname', 'per_nav', 'total_nav', 'nav_rate',

'discount_rate', 'nav_date', 'start_date', 'end_date',

'fund_manager', 'jjlx', 'jjzfe']

NAV_COLUMNS = {'open': NAV_OPEN_COLUMNS,

'close': NAV_CLOSE_COLUMNS, 'grading': NAV_GRADING_COLUMNS}

##########################################################################

# 数据源URL

SINA_NAV_COUNT_URL = '%s%s/fund_center/data/jsonp.php/IO.XSRV2.CallbackList[\'%s\']/NetValue_Service.%s?ccode=&type2=%s&type3=%s'

SINA_NAV_DATA_URL = '%s%s/fund_center/data/jsonp.php/IO.XSRV2.CallbackList[\'%s\']/NetValue_Service.%s?page=%s&num=%s&ccode=&type2=%s&type3=%s'

SINA_NAV_HISTROY_COUNT_URL = '%s%s/fundInfo/api/openapi.php/CaihuiFundInfoService.getNav?symbol=%s&datefrom=%s&dateto=%s'

SINA_NAV_HISTROY_DATA_URL = '%s%s/fundInfo/api/openapi.php/CaihuiFundInfoService.getNav?symbol=%s&datefrom=%s&dateto=%s&num=%s'

SINA_NAV_HISTROY_COUNT_CUR_URL = '%s%s/fundInfo/api/openapi.php/CaihuiFundInfoService.getNavcur?symbol=%s&datefrom=%s&dateto=%s'

SINA_NAV_HISTROY_DATA_CUR_URL = '%s%s/fundInfo/api/openapi.php/CaihuiFundInfoService.getNavcur?symbol=%s&datefrom=%s&dateto=%s&num=%s'

SINA_DATA_DETAIL_URL = '%s%s/quotes_service/api/%s/Market_Center.getHQNodeData?page=1&num=400&sort=symbol&asc=1&node=%s&symbol=&_s_r_a=page'

SINA_FUND_INFO_URL = '%s%s/fundInfo/api/openapi.php/FundPageInfoService.tabjjgk?symbol=%s&format=json'

##########################################################################

DATA_GETTING_TIPS = '[Getting data:]'

DATA_GETTING_FLAG = '#'

DATA_ROWS_TIPS = '%s rows data found.Please wait for a moment.'

DATA_INPUT_ERROR_MSG = 'date input error.'

NETWORK_URL_ERROR_MSG = '获取失败,请检查网络和URL'

DATE_CHK_MSG = '年度输入错误:请输入1989年以后的年份数字,格式:YYYY'

DATE_CHK_Q_MSG = '季度输入错误:请输入1、2、3或4数字'

TOP_PARAS_MSG = 'top有误,请输入整数或all.'

LHB_MSG = '周期输入有误,请输入数字5、10、30或60'

OFT_MSG = u'开放型基金类型输入有误,请输入all、equity、mix、bond、monetary、qdii'

DICT_NAV_EQUITY = {

'fbrq': 'date',

'jjjz': 'value',

'ljjz': 'total',

'change': 'change'

}

DICT_NAV_MONETARY = {

'fbrq': 'date',

'nhsyl': 'value',

'dwsy': 'total',

'change': 'change'

}

import sys

PY3 = (sys.version_info[0] >= 3)

def _write_head():

sys.stdout.write(DATA_GETTING_TIPS)

sys.stdout.flush()

def _write_console():

sys.stdout.write(DATA_GETTING_FLAG)

sys.stdout.flush()

def _write_tips(tip):

sys.stdout.write(DATA_ROWS_TIPS % tip)

sys.stdout.flush()

def _write_msg(msg):

sys.stdout.write(msg)

sys.stdout.flush()

def _check_nav_oft_input(found_type):

if found_type not in NAV_OPEN_KEY.keys():

raise TypeError(OFT_MSG)

else:

return True

def _check_input(year, quarter):

if isinstance(year, str) or year < 1989:

raise TypeError(DATE_CHK_MSG)

elif quarter is None or isinstance(quarter, str) or quarter not in [1, 2, 3, 4]:

raise TypeError(DATE_CHK_Q_MSG)

else:

return True

================================================

FILE: tushare/fund/nav.py

================================================

# -*- coding:utf-8 -*-

"""

获取基金净值数据接口

Created on 2016/04/03

@author: leo

@group : lazytech

@contact: lazytech@sina.cn

"""

from __future__ import division

import time

import json

import re

import pandas as pd

import numpy as np

from tushare.fund import cons as ct

from tushare.util import dateu as du

try:

from urllib.request import urlopen, Request

except ImportError:

from urllib2 import urlopen, Request

def get_nav_open(fund_type='all'):

"""

获取开放型基金净值数据

Parameters

------

type:string

开放基金类型:

1. all 所有开放基金

2. equity 股票型开放基金

3. mix 混合型开放基金

4. bond 债券型开放基金

5. monetary 货币型开放基金

6. qdii QDII型开放基金

return

-------

DataFrame

开放型基金净值数据(DataFrame):

symbol 基金代码

sname 基金名称

per_nav 单位净值

total_nav 累计净值

yesterday_nav 前一日净值

nav_a 涨跌额

nav_rate 增长率(%)

nav_date 净值日期

fund_manager 基金经理

jjlx 基金类型

jjzfe 基金总份额

"""

if ct._check_nav_oft_input(fund_type) is True:

ct._write_head()

nums = _get_fund_num(ct.SINA_NAV_COUNT_URL %

(ct.P_TYPE['http'], ct.DOMAINS['vsf'],

ct.NAV_OPEN_KEY[fund_type],

ct.NAV_OPEN_API[fund_type],

ct.NAV_OPEN_T2[fund_type],

ct.NAV_OPEN_T3))

pages = 2 # 分两次请求数据

limit_cnt = int(nums/pages)+1 # 每次取的数量

fund_dfs = []

for page in range(1, pages+1):

fund_dfs = _parse_fund_data(ct.SINA_NAV_DATA_URL %

(ct.P_TYPE['http'], ct.DOMAINS['vsf'],

ct.NAV_OPEN_KEY[fund_type],

ct.NAV_OPEN_API[fund_type],

page,

limit_cnt,

ct.NAV_OPEN_T2[fund_type],

ct.NAV_OPEN_T3))

return pd.concat(fund_dfs, ignore_index=True)

def get_nav_close(fund_type='all', sub_type='all'):

"""

获取封闭型基金净值数据

Parameters

------

type:string

封闭基金类型:

1. all 所有封闭型基金

2. fbqy 封闭-权益

3. fbzq 封闭债券

sub_type:string

基金子类型:

1. type=all sub_type无效

2. type=fbqy 封闭-权益

*all 全部封闭权益

*ct 传统封基

*cx 创新封基

3. type=fbzq 封闭债券

*all 全部封闭债券

*wj 稳健债券型

*jj 激进债券型

*cz 纯债债券型

return

-------

DataFrame

开放型基金净值数据(DataFrame):

symbol 基金代码

sname 基金名称

per_nav 单位净值

total_nav 累计净值

nav_rate 增长率(%)

discount_rate 折溢价率(%)

nav_date 净值日期

start_date 成立日期

end_date 到期日期

fund_manager 基金经理

jjlx 基金类型

jjzfe 基金总份额

"""

ct._write_head()

nums = _get_fund_num(ct.SINA_NAV_COUNT_URL %

(ct.P_TYPE['http'], ct.DOMAINS['vsf'],

ct.NAV_CLOSE_KEY, ct.NAV_CLOSE_API,

ct.NAV_CLOSE_T2[fund_type],

ct.NAV_CLOSE_T3[sub_type]))

fund_df = _parse_fund_data(ct.SINA_NAV_DATA_URL %

(ct.P_TYPE['http'], ct.DOMAINS['vsf'],

ct.NAV_OPEN_KEY, ct.NAV_CLOSE_API,

ct.NAV_DEFAULT_PAGE,

nums,

ct.NAV_CLOSE_T2[fund_type],

ct.NAV_CLOSE_T3[sub_type]),

'close')

return fund_df

def get_nav_grading(fund_type='all', sub_type='all'):

"""

获取分级子基金净值数据

Parameters

------

type:string

封闭基金类型:

1. all 所有分级基金

2. fjgs 分级-固收

3. fjgg 分级-杠杆

sub_type:string

基金子类型(type=all sub_type无效):

*all 全部分级债券

*wjzq 稳健债券型

*czzq 纯债债券型

*jjzq 激进债券型

*gp 股票型

*zs 指数型

return

-------

DataFrame

开放型基金净值数据(DataFrame):

symbol 基金代码

sname 基金名称

per_nav 单位净值

total_nav 累计净值

nav_rate 增长率(%)

discount_rate 折溢价率(%)

nav_date 净值日期

start_date 成立日期

end_date 到期日期

fund_manager 基金经理

jjlx 基金类型

jjzfe 基金总份额

"""

ct._write_head()

nums = _get_fund_num(ct.SINA_NAV_COUNT_URL %

(ct.P_TYPE['http'], ct.DOMAINS['vsf'],

ct.NAV_GRADING_KEY, ct.NAV_GRADING_API,

ct.NAV_GRADING_T2[fund_type],

ct.NAV_GRADING_T3[sub_type]))

fund_df = _parse_fund_data(ct.SINA_NAV_DATA_URL %

(ct.P_TYPE['http'], ct.DOMAINS['vsf'],

ct.NAV_GRADING_KEY, ct.NAV_GRADING_API,

ct.NAV_DEFAULT_PAGE,

nums,

ct.NAV_GRADING_T2[fund_type],

ct.NAV_GRADING_T3[sub_type]),

'grading')

return fund_df

def get_nav_history(code, start=None, end=None, retry_count=3, pause=0.001, timeout=10):

'''

获取历史净值数据

Parameters

------

code:string

基金代码 e.g. 000001

start:string

开始日期 format:YYYY-MM-DD 为空时取当前日期

end:string

结束日期 format:YYYY-MM-DD 为空时取去年今日

retry_count : int, 默认 3

如遇网络等问题重复执行的次数

pause : int, 默认 0

重复请求数据过程中暂停的秒数,防止请求间隔时间太短出现的问题

timeout: int 默认 10s

请求大量数据时的网络超时

return

-------

DataFrame

date 发布日期 (index)

value 基金净值(股票/混合/QDII型基金) / 年华收益(货币/债券基金)

total 累计净值(股票/混合/QDII型基金) / 万分收益(货币/债券基金)

change 净值增长率(股票/混合/QDII型基金)

'''

start = du.today_last_year() if start is None else start

end = du.today() if end is None else end

# 判断基金类型

ismonetary = False # 是否是债券型和货币型基金

df_fund = get_fund_info(code)

fund_type = df_fund.ix[0]['Type2Name']

if (fund_type.find(u'债券型') != -1) or (fund_type.find(u'货币型') != -1):

ismonetary = True

ct._write_head()

nums = _get_nav_histroy_num(code, start, end, ismonetary)

data = _parse_nav_history_data(

code, start, end, nums, ismonetary, retry_count, pause, timeout)

return data

def get_fund_info(code):

'''

获取基金基本信息

Parameters

------

code:string

基金代码 e.g. 000001

return

-------

DataFrame

jjqc 基金全称

jjjc 基金简称

symbol 基金代码

clrq 成立日期

ssrq 上市日期

xcr 存续期限

ssdd 上市地点

Type1Name 运作方式

Type2Name 基金类型

Type3Name 二级分类

jjgm 基金规模(亿元)

jjfe 基金总份额(亿份)

jjltfe 上市流通份额(亿份)

jjferq 基金份额日期

quarter 上市季度

glr 基金管理人

tgr 基金托管人

'''

request = ct.SINA_FUND_INFO_URL % (

ct.P_TYPE['http'], ct.DOMAINS['ssf'], code)

text = urlopen(request, timeout=10).read()

text = text.decode('gbk')

org_js = json.loads(text)

status_code = int(org_js['result']['status']['code'])

if status_code != 0:

status = str(org_js['result']['status']['msg'])

raise ValueError(status)

data = org_js['result']['data']

fund_df = pd.DataFrame(data, columns=ct.FUND_INFO_COLS, index=[0])

fund_df = fund_df.set_index('symbol')

return fund_df

def _parse_fund_data(url, fund_type='open'):

ct._write_console()

try:

request = Request(url)

text = urlopen(request, timeout=10).read()

if text == 'null':

return None

text = text.decode('gbk') if ct.PY3 else text

text = text.split('data:')[1].split(',exec_time')[0]

reg = re.compile(r'\,(.*?)\:')

text = reg.sub(r',"\1":', text)

text = text.replace('"{symbol', '{"symbol')

text = text.replace('{symbol', '{"symbol"')

if ct.PY3:

jstr = json.dumps(text)

else:

jstr = json.dumps(text, encoding='gbk')

org_js = json.loads(jstr)

fund_df = pd.DataFrame(pd.read_json(org_js, dtype={'symbol': object}),

columns=ct.NAV_COLUMNS[fund_type])

fund_df.fillna(0, inplace=True)

return fund_df

except Exception as er:

print(str(er))

def _get_fund_num(url):

"""

获取基金数量

"""

ct._write_console()

try:

request = Request(url)

text = urlopen(request, timeout=10).read()

text = text.decode('gbk')

if text == 'null':

raise ValueError('get fund num error')

text = text.split('((')[1].split('))')[0]

reg = re.compile(r'\,(.*?)\:')

text = reg.sub(r',"\1":', text)

text = text.replace('{total_num', '{"total_num"')

text = text.replace('null', '0')

org_js = json.loads(text)

nums = org_js["total_num"]

return int(nums)

except Exception as er:

print(str(er))

def _get_nav_histroy_num(code, start, end, ismonetary=False):

"""

获取基金历史净值数量

--------

货币和证券型基金采用的url不同,需要增加基金类型判断

"""

ct._write_console()

if ismonetary:

request = Request(ct.SINA_NAV_HISTROY_COUNT_CUR_URL %

(ct.P_TYPE['http'], ct.DOMAINS['ssf'],

code, start, end))

else:

request = Request(ct.SINA_NAV_HISTROY_COUNT_URL %

(ct.P_TYPE['http'], ct.DOMAINS['ssf'],

code, start, end))

text = urlopen(request, timeout=10).read()

text = text.decode('gbk')

org_js = json.loads(text)

status_code = int(org_js['result']['status']['code'])

if status_code != 0:

status = str(org_js['result']['status']['msg'])

raise ValueError(status)

nums = org_js['result']['data']['total_num']

return int(nums)

def _parse_nav_history_data(code, start, end, nums, ismonetary=False, retry_count=3, pause=0.01, timeout=10):

if nums == 0:

return None

for _ in range(retry_count):

time.sleep(pause)

# try:

ct._write_console()

if ismonetary:

request = Request(ct.SINA_NAV_HISTROY_DATA_CUR_URL %

(ct.P_TYPE['http'], ct.DOMAINS['ssf'],

code, start, end, nums))

else:

request = Request(ct.SINA_NAV_HISTROY_DATA_URL %

(ct.P_TYPE['http'], ct.DOMAINS['ssf'],

code, start, end, nums))

text = urlopen(request, timeout=timeout).read()

text = text.decode('gbk')

org_js = json.loads(text)

status_code = int(org_js['result']['status']['code'])

if status_code != 0:

status = str(org_js['result']['status']['msg'])

raise ValueError(status)

data = org_js['result']['data']['data']

if 'jjjz' in data[0].keys():

fund_df = pd.DataFrame(data, columns=ct.NAV_HIS_JJJZ)

fund_df['jjjz'] = fund_df['jjjz'].astype(float)

fund_df['ljjz'] = fund_df['ljjz'].astype(float)

fund_df.rename(columns=ct.DICT_NAV_EQUITY, inplace=True)

else:

fund_df = pd.DataFrame(data, columns=ct.NAV_HIS_NHSY)

fund_df['nhsyl'] = fund_df['nhsyl'].astype(float)

fund_df['dwsy'] = fund_df['dwsy'].astype(float)

fund_df.rename(columns=ct.DICT_NAV_MONETARY, inplace=True)

#fund_df.fillna(0, inplace=True)

if fund_df['date'].dtypes == np.object:

fund_df['date'] = pd.to_datetime(fund_df['date'])

fund_df = fund_df.set_index('date')

fund_df = fund_df.sort_index(ascending=False)

fund_df['pre_value'] = fund_df['value'].shift(-1)

fund_df['change'] = (fund_df['value'] / fund_df['pre_value'] - 1) * 100

fund_df = fund_df.drop('pre_value', axis=1)

return fund_df

raise IOError(ct.NETWORK_URL_ERROR_MSG)

================================================

FILE: tushare/futures/__init__.py

================================================

================================================

FILE: tushare/futures/cons.py

================================================

#!/usr/bin/env python

# -*- coding:utf-8 -*-

'''

Created on 2016年10月17日

@author: Jimmy Liu

@group : waditu

@contact: jimmysoa@sina.cn

'''

P_TYPE = {'http': 'http://', 'ftp': 'ftp://'}

DOMAINS = {

'EM': 'eastmoney.com'

}

PAGES = {'INTL_FUT': 'index.aspx'}

INTL_FUTURE_CODE = 'CONX0,GLNZ0,LCPS0,SBCX0,CRCZ0,WHCZ0,SMCZ0,SOCZ0,CTNZ0,HONV0,LALS0,LZNS0,LTNS0,LNKS0,LLDS0,RBTZ0,SBCC0,SMCC0,SOCC0,WHCC0,SGNC0,SFNC0,CTNC0,CRCC0,CCNC0,CFNC0,GLNC0,CONC0,HONC0,RBTC0,OILC0'

INTL_FUTURE_URL = '%shq2gjqh.%s/EM_Futures2010NumericApplication/%s?type=z&jsName=quote_future&sortType=A&sortRule=1&jsSort=1&ids=%s&_g=0.%s'

INTL_FUTURES_COL = ['code', 'name', 'price', 'open', 'high', 'low', 'preclose', 'vol', 'pct_count', 'pct_change', 'posi', 'b_amount', 's_amount']

================================================

FILE: tushare/futures/domestic.py

================================================

#!/usr/bin/env python

# -*- coding:utf-8 -*-

'''

Created on 2017年06月04日

@author: debugo

@contact: me@debugo.com

'''

import json

import datetime

from bs4 import BeautifulSoup

import pandas as pd

from tushare.futures import domestic_cons as ct

try:

from urllib.request import urlopen, Request

from urllib.parse import urlencode

from urllib.error import HTTPError

from http.client import IncompleteRead

except ImportError:

from urllib import urlencode

from urllib2 import urlopen, Request

from urllib2 import HTTPError

from httplib import IncompleteRead

def get_cffex_daily(date = None):

"""

获取中金所日交易数据

Parameters

------

date: 日期 format:YYYY-MM-DD 或 YYYYMMDD 或 datetime.date对象 为空时为当天

Return

-------

DataFrame

中金所日交易数据(DataFrame):

symbol 合约代码

date 日期

open 开盘价

high 最高价

low 最低价

close 收盘价

volume 成交量

open_interest 持仓量

turnover 成交额

settle 结算价

pre_settle 前结算价

variety 合约类别

或 None(给定日期没有交易数据)

"""

day = ct.convert_date(date) if date is not None else datetime.date.today()

try:

html = urlopen(Request(ct.CFFEX_DAILY_URL % (day.strftime('%Y%m'),

day.strftime('%d'), day.strftime('%Y%m%d')),

headers=ct.SIM_HAEDERS)).read().decode('gbk', 'ignore')

except HTTPError as reason:

if reason.code != 404:

print(ct.CFFEX_DAILY_URL % (day.strftime('%Y%m'), day.strftime('%d'),

day.strftime('%Y%m%d')), reason)

return

if html.find(u'网页错误') >= 0:

return

html = [i.replace(' ','').split(',') for i in html.split('\n')[:-2] if i[0][0] != u'小' ]

if html[0][0]!=u'合约代码':

return

dict_data = list()

day_const = day.strftime('%Y%m%d')

for row in html[1:]:

m = ct.FUTURE_SYMBOL_PATTERN.match(row[0])

if not m:

continue

row_dict = {'date': day_const, 'symbol': row[0], 'variety': m.group(1)}

for i,field in enumerate(ct.CFFEX_COLUMNS):

if row[i+1] == u"":

row_dict[field] = 0.0

elif field in ['volume', 'open_interest', 'oi_chg']:

row_dict[field] = int(row[i+1])

else:

row_dict[field] = float(row[i+1])

row_dict['pre_settle'] = row_dict['close'] - row_dict['change1']

dict_data.append(row_dict)

return pd.DataFrame(dict_data)[ct.OUTPUT_COLUMNS]

def get_czce_daily(date=None, type="future"):

"""

获取郑商所日交易数据

Parameters

------

date: 日期 format:YYYY-MM-DD 或 YYYYMMDD 或 datetime.date对象 为空时为当天

type: 数据类型, 为'future'期货 或 'option'期权二者之一

Return

-------

DataFrame

郑商所每日期货交易数据:

symbol 合约代码

date 日期

open 开盘价

high 最高价

low 最低价

close 收盘价

volume 成交量

open_interest 持仓量

turnover 成交额

settle 结算价

pre_settle 前结算价

variety 合约类别

或

DataFrame

郑商所每日期权交易数据

symbol 合约代码

date 日期

open 开盘价

high 最高价

low 最低价

close 收盘价

pre_settle 前结算价

settle 结算价

delta 对冲值

volume 成交量

open_interest 持仓量

oi_change 持仓变化

turnover 成交额

implied_volatility 隐含波动率

exercise_volume 行权量

variety 合约类别

None(类型错误或给定日期没有交易数据)

"""

if type == 'future':

url = ct.CZCE_DAILY_URL

listed_columns = ct.CZCE_COLUMNS

output_columns = ct.OUTPUT_COLUMNS

elif type == 'option':

url = ct.CZCE_OPTION_URL

listed_columns = ct.CZCE_OPTION_COLUMNS

output_columns = ct.OPTION_OUTPUT_COLUMNS

else:

print('invalid type :' + type + ',type should be one of "future" or "option"')

return

day = ct.convert_date(date) if date is not None else datetime.date.today()

try:

html = urlopen(Request(url % (day.strftime('%Y'),

day.strftime('%Y%m%d')),

headers=ct.SIM_HAEDERS)).read().decode('gbk', 'ignore')

except HTTPError as reason:

if reason.code != 404:

print(ct.CZCE_DAILY_URL % (day.strftime('%Y'),

day.strftime('%Y%m%d')), reason)

return

if html.find(u'您的访问出错了') >= 0 or html.find(u'无期权每日行情交易记录') >= 0:

return

html = [i.replace(' ','').split('|') for i in html.split('\n')[:-4] if i[0][0] != u'小']

if html[1][0] not in [u'品种月份', u'品种代码']:

return

dict_data = list()

day_const = int(day.strftime('%Y%m%d'))

for row in html[2:]:

m = ct.FUTURE_SYMBOL_PATTERN.match(row[0])

if not m:

continue

row_dict = {'date': day_const, 'symbol': row[0], 'variety': m.group(1)}

for i,field in enumerate(listed_columns):

if row[i+1] == "\r":

row_dict[field] = 0.0

elif field in ['volume', 'open_interest', 'oi_chg', 'exercise_volume']:

row[i+1] = row[i+1].replace(',','')

row_dict[field] = int(row[i+1])

else:

row[i+1] = row[i+1].replace(',','')

row_dict[field] = float(row[i+1])

dict_data.append(row_dict)

return pd.DataFrame(dict_data)[output_columns]

def get_shfe_vwap(date = None):

"""

获取上期所日成交均价数据

Parameters

------

date: 日期 format:YYYY-MM-DD 或 YYYYMMDD 或 datetime.date对象 为空时为当天

Return

-------

DataFrame

郑商所日交易数据(DataFrame):

symbol 合约代码

date 日期

time_range vwap时段,分09:00-10:15和09:00-15:00两类

vwap 加权平均成交均价

或 None(给定日期没有数据)

"""

day = ct.convert_date(date) if date is not None else datetime.date.today()

try:

json_data = json.loads(urlopen(Request(ct.SHFE_VWAP_URL % (day.strftime('%Y%m%d')),

headers=ct.SIM_HAEDERS)).read().decode('utf8'))

except HTTPError as reason:

if reason.code != 404:

print(ct.SHFE_DAILY_URL % (day.strftime('%Y%m%d')), reason)

return

if len(json_data['o_currefprice']) == 0:

return

df = pd.DataFrame(json_data['o_currefprice'])

df['INSTRUMENTID'] = df['INSTRUMENTID'].str.strip()

df[':B1'].astype('int16')

return df.rename(columns=ct.SHFE_VWAP_COLUMNS)[list(ct.SHFE_VWAP_COLUMNS.values())]

def get_shfe_daily(date = None):

"""

获取上期所日交易数据

Parameters

------

date: 日期 format:YYYY-MM-DD 或 YYYYMMDD 或 datetime.date对象 为空时为当天

Return

-------

DataFrame

上期所日交易数据(DataFrame):

symbol 合约代码

date 日期

open 开盘价

high 最高价

low 最低价

close 收盘价

volume 成交量

open_interest 持仓量

turnover 成交额

settle 结算价

pre_settle 前结算价

variety 合约类别

或 None(给定日期没有交易数据)

"""

day = ct.convert_date(date) if date is not None else datetime.date.today()

try:

json_data = json.loads(urlopen(Request(ct.SHFE_DAILY_URL % (day.strftime('%Y%m%d')),

headers=ct.SIM_HAEDERS)).read().decode('utf8'))

except HTTPError as reason:

if reason.code != 404:

print(ct.SHFE_DAILY_URL % (day.strftime('%Y%m%d')), reason)

return

if len(json_data['o_curinstrument']) == 0:

return

df = pd.DataFrame([row for row in json_data['o_curinstrument'] if row['DELIVERYMONTH'] != u'小计' and row['DELIVERYMONTH'] != ''])

df['variety'] = df.PRODUCTID.str.slice(0, -6).str.upper()

df['symbol'] = df['variety'] + df['DELIVERYMONTH']

df['date'] = day.strftime('%Y%m%d')

vwap_df = get_shfe_vwap(day)

if vwap_df is not None:

df = pd.merge(df, vwap_df[vwap_df.time_range == '9:00-15:00'], on=['date', 'symbol'], how='left')

df['turnover'] = df.vwap * df.VOLUME

else:

print('Failed to fetch SHFE vwap.', day.strftime('%Y%m%d'))

df['turnover'] = .0

df.rename(columns=ct.SHFE_COLUMNS, inplace=True)

return df[ct.OUTPUT_COLUMNS]

def get_dce_daily(date = None, type="future", retries=0):

"""

获取大连商品交易所日交易数据

Parameters

------

date: 日期 format:YYYY-MM-DD 或 YYYYMMDD 或 datetime.date对象 为空时为当天

type: 数据类型, 为'future'期货 或 'option'期权二者之一

retries: int, 当前重试次数,达到3次则获取数据失败

Return

-------

DataFrame

大商所日交易数据(DataFrame):

symbol 合约代码

date 日期

open 开盘价